Pollen Street Capital Group Best Execution Policy

Glossary

| Terms | Definitions |

|---|---|

| Advisers Act | The Investment Advisers Act of 1940 |

| AIFMD | The Alternative Investment Fund Managers Directive |

| AIFM | The Alternative Investment Fund Manager |

| AIF(s) | Alternative Investment Funds and has the meaning as set out in Article 4 of the AIFMD |

| AML | Anti-Money Laundering |

| Associated Persons | includes any agent of the Management Group or any other person who performs services for or on behalf of the Management Group and includes all those individuals falling within the definition of Staff Members and Group Fund |

| CISI | Chartered Institute for Securities & Investment |

| Client | references in this policy to Client are to any fund for which the PSC Managers act |

| ComplySci | A compliance system utilised by the Management Group for all compliance related items. The system may be accessed here. |

| Compliance Officer | Has the meaning of the FCA designated Compliance Oversight Function (SMF16) |

| CPMI | Collective Portfolio Management Investment Firm |

| CSA | Credit Support Annex |

| ExCo | Executive Committee |

| Execution Venues | a regulated market, an MTF, an OTF, a systematic internaliser, or a market maker or other liquidity provider or an entity that performs a similar function in a third country to the functions performed by any of the foregoing. |

| FCA | Financial Conduct Authority |

|

Financial Instruments |

transferable securities; money-market instruments; units in collective investment undertakings; options, futures, swaps, forward rate agreements and any other derivative contracts relating to securities, currencies, interest rates or yields, emission allowances, or other derivative instruments, financial indices or financial measures which may be settled physically or in cash; |

| GRC | Group Risk Committee |

| Group Fund | any of the Management Group’s staff appointed as a director of a company in which a fund managed or advised by the Management Group has made an investment |

| Investment Committee | Each Client will have its own investment committee whose members will be charged with making investment decisions on its behalf. For those Clients for which the Group acts as the investment adviser, the relevant General Partner will be responsible for making the final decision after being advised by the relevant PSC Manager. |

| MiFID II | The Markets in Financial Instruments Directive II 2014/65/EU |

| MLRO | The Money Laundering Reporting Officer as designated by the FCA for oversight of a firm’s compliance with the FCA’s rules on systems and controls against money laundering |

|

Multilateral Trading Facility (MTF) |

a multilateral system, operated by an investment firm or a market operator, which brings together multiple third party buying and selling interests in financial instruments – in the system and in accordance with non-discretionary rules – in a way that results in a contract. |

| Nominated Officer | Person designated under the MLR to receive suspicious activity reports |

|

Organised Trading Facility (OTF) |

a multilateral system that is not a RM or MTF. Within an OTF, multiple third-party buying and selling interests in bonds, structured finance products, emission allowances or derivatives are able to interact in a way that results in a contract. Equities are not permitted to be traded through an OTF. |

| PSC Group | Has the meaning of Pollen Street plc and all its subsidiaries |

| PSC Managers | Pollen Street Capital Limited ("PSCL"), PSC Credit Holdings LLP ("PSCCH"), Pollen Street Capital (US) LLC. |

| PSC US | Pollen Street Capital (US) LLC as investment adviser |

| Regulated Entities of the Management Group | Has the meaning of the following entities: - Pollen Street Capital Limited - PSC Credit Holdings LLP - Honeycomb Finance Limited - AvantCredit of UK, LLC |

| Regulated Market (RM) | means a multilateral system operated and/or managed by a market operator, which brings together or facilities the bringing together of multiple third party buying and selling interests in financial instruments – in the system and in accordance with its non-discretionary rules – in a way that results in a contract, in respect of the financial instruments admitted to trading under its rules and /or systems, and which is authorised and functions regularly |

| SEC | U.S. Securities and Exchange Commission |

| Staff, Staff Members | Includes directors, partners, employees, contractors, consultants, agency workers, seconded workers and interns |

| Systematic Internaliser | an investment firm which, on an organised, frequent and systematic basis, deals on its own account by executing client orders outside a Regulated Market, MTF or OFT |

1. Scope

This policy applies to members of Staff in PSC Managers.

2. Introduction

This Policy applies to the PSC Managers who are subject to FCA’s and/or the SEC’s best execution requirements. PSCL and PSCCH, as CPMI firms, have an obligation to follow the rules under AIFMD in respect of best execution when managing AIFs, and MiFID II when providing portfolio management services. For ease of process, the Managers will comply with the MiFID requirements in relation to order execution and will be required to take all sufficient steps to obtain the best possible results for their Clients taking into account the execution factors. As part of the Managers’ fiduciary duty to their Clients, the Managers have an obligation to trade assets in a manner and on terms most favourable to their Clients, and to exercise diligence and care throughout the trading process.

Trading in financial instruments is not part of the core investment strategy of the Management Group’s Clients, however, the Managers may on occasion execute financial instruments for treasury management purposes and to the extent permitted by the offering documents of the Clients as part of the portfolio construction.

The Best Execution policy has been established to ensure sound, transparent and comprehensive execution processes are followed and specifies the controls and safeguards that are in place.

The Executive Committee is responsible for ensuring that robust business practices are operating in all its trading activities to deliver Best Execution on a consistent basis and for promoting a culture that proactively identifies and manages conflicts of interest. This responsibility is delegated to the GRC who is responsible for the review and monitoring of this Policy, to ensure that it remains robust and fit for purpose, taking into account, amongst other things, changes to market structures and execution practices and development of new products. ExCo maintains oversight of this process and receives regular reports from the GRC on this matter.

Upon request, the Managers will provide appropriate information about this Policy to their Clients.

3. Policy Review

The Managers’ Compliance Officers and the Head of Treasury Management are responsible for the maintenance and annual review of this Policy and the Managers’ Best Execution procedures. The review focuses on whether the Managers would obtain better results for their Clients if they were to:

- include additional or remove existing execution venues or brokers;

- assign a different relative importance to the Execution Factors applicable to each financial instrument class; or

- modify any other aspects of this Policy and/or the Managers’ Best Execution procedures.

The review takes into account a number of factors including:

- any deficiencies with this Policy and/or the Managers’ execution procedures identified during the monitoring processes;

- any factors that could damage the quality of execution being achieved, such as changes in the market environment and structure (e.g. the entry or exit of market participants, changes to execution venues, services provided by counterparties, significant changes in technology, etc.);

- changes to the types of investment process used;

- changes to the financial instruments used and/or introduction of new products;

- changes to the nature of orders; and

- changes in relevant legislation

In addition, this Policy and/or the Managers’ Best Execution procedures are reviewed whenever a material change occurs in the market that could affect the Managers’ ability to obtain the best possible result for the execution of their Clients' orders.

The Managers’ review also takes into account a review of the monitoring program to ensure that monitoring processes remain fit for purpose and appropriate.

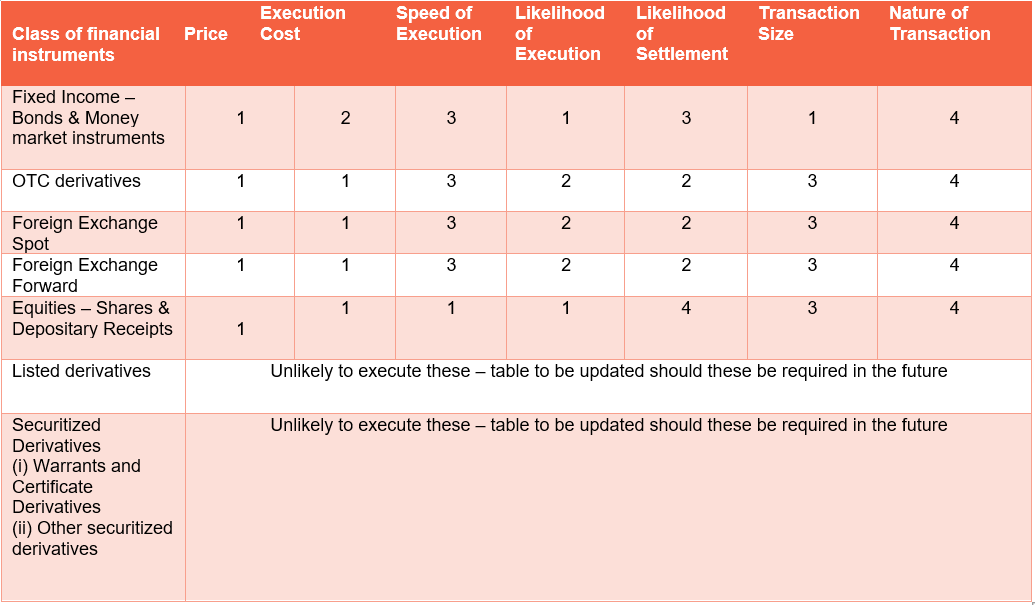

4. Execution Factors

This Policy is designed to obtain the best possible results for each Client, taking into account any specific requirement of the Client that orders are being executed on behalf of, the priorities of the Client and the nature of the markets and products in question.

In order to deliver Best Execution, the Managers use their knowledge, experience and judgement to execute trades on behalf of their Clients, taking into consideration a number of execution factors including:

- The price that the order can be executed at;

- The costs of execution of the transaction to the Client;

- The speed of execution of the transaction;

- The likelihood of achieving execution and settlement;

- The size of the order; and

- Any other relevant factors specific to the execution of the specific order (the “Execution Factors”).

5. Execution Criteria

The Managers are required to determine the relative importance of the Execution Factors for their Clients by taking into account the following criteria:

- The characteristics of each Client including the categorisation of the client;

- The characteristics of the Client order including where the order involves a securities financing transaction (SFT);;

- The characteristics of the financial instruments that are the subject of that order;

- The characteristics of the execution venues/brokers to which that order can be directed; and, where relevant

- For each Client under management, the objectives, investment policy and risks specific to the Client, as indicated in the constituting documents, articles of association or offering documents (the “Execution Criteria”).

6. Execution Venues and Brokers

The Managers will primarily select the execution venue or broker that, in the Managers’ judgment, is the most appropriate, taking into account the Execution Factors and Execution Criteria. The Managers will also consider the market coverage and market intelligence that the execution venue or broker can provide, such that this will aid the Best Execution of Client orders.

The Managers do not execute on a Direct Market Access (“DMA”) basis, and therefore will always use a broker / market maker to execute trades in financial instruments. These trades may result in the broker / market maker executing a trade with a 3rd party unknown to the Managers, but the considerations of that onward execution do not directly form part of the consideration of this Policy.

When determining the approach to achieve Best Execution, the individual responsible for executing trades must determine which broker or execution venue to use (where more than one is available for a particular financial instrument). The Managers will consider the cost and commission implications of each method where there are competing options.

The execution venues that the Managers may use are:

- Regulated markets

- Multilateral Trading Facilities (“MTF”)

- Organised Trading Facilities (“OTF”)

- Market makers/Systematic Internalisers (“SIs”)

- Portfolio companies as affiliated brokers

Depending on the class of financial instrument, the Managers may execute Client orders outside a Trading Venue, including through bilateral counterparties, for which prior Client consent will be sought by way of a general agreement. Orders executed outside of a Trading Venue are executed under industry legal documentation such as an International Swaps and Derivatives Association (ISDA) master agreement and Credit Support Annex (CSA) or Credit Support Deed (CSD).The Group is responsible for reviewing and approving all trading counterparties used by the Managers for the purpose of order execution and may add or remove counterparties as deemed appropriate.

In exceptional circumstances, PSC may use a venue or entity not currently listed in this policy so as to fulfil its overarching best execution requirement to take all reasonable steps to obtain the best possible result for the execution of client orders, taking into account the best execution factors.

The list of trading counterparties used by the Managers can be found in Appendix 1.

The Managers have identified above those venues on which they most regularly seek to execute and which the Managers believe offer the best prospects for affording their Clients Best Execution.

In selecting the most appropriate venues for the purpose of executing orders, the Managers will take into full account the Execution Factors and Execution Criteria relevant to the order, and the following:

- what the Managers reasonably assess to be in the best interest of the Clients in terms of executing the orders; and

- such other factors as may be appropriate, including the ability of the venue to manage complex orders, the speed of execution, the creditworthiness of the venue and the quality of any related clearing and settlement facilities.

The diversity in the markets and instruments in which the Managers trade and the kind of orders that the Client may place mean that different factors will have to be taken into account when the Managers assess the nature of its Policy in the context of different instruments and different markets. In some markets, price volatility may mean that the timeliness of execution is a priority, whereas, in other markets that have low liquidity, the fact of execution may itself constitute Best Execution. In other cases, the Managers choice of venue may be limited (even to the fact that there may only be one platform/market upon which the Managers can execute Client orders) because of the nature of the Client order or of specific Client requirements.

7. Selection of Brokers

In determining whether a broker is qualified to provide services to the Managers’ Clients, the Manager consider, among others, the following relevant factors:

- Regulatory status / checks

- Nature and size of the transactions in the ordinary course of business

- Financial status / checks / any minimum capitalisation thresholds

- Ability to maintain the confidentiality of trading intentions

- Timeliness and certainty of execution

- Expertise as it relates to instruments executed by the Manager

- Market intelligence

- Efficient execution and competence in supporting the trade execution process

- Depth of client base

- Ability to manage conflicts of interest

- Business reputation

- Credibility and reputation

The Managers have complete discretion in selecting the broker that they use for transactions and the commission rates that Clients pay such brokers where applicable. The Managers’ overriding objective in effecting transactions is to seek to obtain the best overall result in the execution of its Clients’ orders. It is not necessary to select the broker offering the lowest commission rate. The Manager may cause a Client to pay a broker a commission in excess of that which another broker might have charged for effecting the same transaction in recognition of the value of the brokerage and other services provided by the broker, or there may be other economics in the transaction other than purely the commission rate e.g. margin requirements.

PSC Managers will monitor conflicts of interests at all times and will ensure they do not receive any remuneration, discounts or non-monetary benefits, such as gifts and entertainment, for directing Client orders to an execution venue.

The Managers may select a single entity for execution only where they are able to show that this provides the best possible result for their Clients on a consistent basis, and where they can reasonably expect that the selected entity will enable them to obtain results for Clients that are at least as good as the results that could reasonably be expected from using alternative entities for execution. In some circumstances, the Managers may only have one trading counterparty available to them as a result of the limited scope of trading activity undertaken.

8. Instruments

8.1 Execution Factors: Bonds

The process by which the decision as to the appropriate venue on which to execute any bond transaction will depend mostly on the instrument being executed, but also the reason for the trade (e.g. change in Investment Committee risk appetite, portfolio concentrations, liquidity etc…). Each instrument will have a limited number of execution options, and at any time there may be factors influencing those options which make them more or less attractive in terms of being able to obtain the best pricing. While price will generally be the most important factor, certainty of execution may rank highly or even at times be of greater importance. Where price is of priority over other execution factors, sufficient efforts should be made to achieve a minimum of 3 pricing quotes, where available, to ensure that Best Execution is achieved. This might not always be possible, for instance, where there may be some sensitivity around executing the trade, limited liquidity in the instrument, lack of general market liquidity or other sensitivity in executing the trade, either from a wider market perspective or specific to one of the Managers’ Clients.

8.2 Execution Factors: Money Market Instruments

All foreign exchange transactions will be for hedging purposes only (not trading positions). The overall economics will be considered including price, credit charges and margin costs.

Often ISDAs/CSAs or other standard terms may be necessary to have in place prior to trading, which may limit the number of available counterparties. In such instances, the likelihood of achieving execution and settlement will be prioritised as an execution factor.

8.3 Execution Factors: Foreign Exchange

All foreign exchange transactions will be for hedging purposes only (not trading positions). The overall economics will be considered including price, credit charges and margin costs.

Often ISDAs/CSAs or other standard terms may be necessary to have in place prior to trading, which may limit the number of available counterparties. In such instances, the likelihood of achieving execution and settlement will be prioritised as an execution factor.

8.4 Execution Factors: OTC Derivatives

Dealing in OTC derivatives will be limited to pre-authorised counterparties with whom ISDA/CSA agreements or other standard terms of business are in place, and in such cases the perceived operational efficiency of such counterparties will be relevant. Execution will tend to depend on, amongst others, price, overall trade economics taking into consideration margin requirements, size of transaction, liquidity, counterparty risk, credit risk and perceived settlement capabilities.

The Managers do not currently trade in exchange-traded derivatives.

8.5 Execution Factors: Equities

Dealing in equities does not form part of the core strategy of the Clients and, as such, will be on a limited basis. Decisions to trade in equities will be taken by the Investment Committee and would be ad-hoc in nature, such as a post-IPO sell down. The Investment Committee will be responsible for assessing the nature of the relevant transaction and determining which execution factors to prioritise. As such, the relative importance of the execution factors will be subject to the characteristics of the client order.

8.6 Execution Factors: Portfolio Companies

Where portfolio companies of the Group’s Clients offer any of the services above, the Managers may use these services, subject to the conflicts of interest policy (as applicable), such that Clients get the best result as a whole.

9. Execution Quality

The PSC Managers will monitor the execution quality of the entities identified in this policy and, where appropriate, correct any deficiencies. As part of this review, the Managers assess whether a material change has occurred and will consider making changes to the execution venues or entities on which they place significant reliance in meeting the overarching best execution requirement.

10. Senior Management and Escalation

The Managers are responsible for ensuring that robust business practices are operating in all trading activities to deliver Best Execution on a consistent basis and for promoting a culture that proactively identifies and manages conflicts of interest. The Managers’ Board is also ultimately responsible for the on-going review and monitoring of this Policy, to ensure that it remains robust and fit for purpose, taking into account, amongst other things, changes to market structures and execution practices and development of new products.

Any deficiencies or issues identified by the Managers’ as part of its monitoring of the quality of execution should be reported to the Group Risk Committee, in the first instance, for its review with sufficient detail and a proposal for corrective action to be taken, including any proposed changes to this Policy. Any material policy changes will be validated by the Board.

11. Research and Inducements

In the UK, some firms are required to comply with the research rules on inducements when executing orders, or placing orders with other entities for execution, that relate to financial instruments for, or on behalf of, a fund. Such firms would not be able to accept research that is paid for by a third party, e.g. a broker, as this would be deemed an inducement.

The UK Managers will not be subject to this requirement as they are able rely on the following exemption which states that the rules on research and inducements do not apply in relation to a fund which, in accordance with its core investment policy:

- Does not generally invest in financial instruments that can be:

- (a) registered in a financial instruments account opened in the books of a depositary; or

- (b) physically delivered to the depositary; or

- Generally, invests in issuers or non-listed companies to potentially acquire control over such companies either individually or jointly with other funds.

PSCUS does not presently utilize soft dollars. In the event that PSCUS utilizes soft dollars, it will do so solely to pay for products or services that qualify as “research and brokerage services” within the meaning of Section 28(e) of the Securities Exchange Act of 1934, as amended (the “1934 Act”). Compliance approval is required prior to the firm engaging in soft dollar/CSA arrangements.

12. MiFID Ongoing Obligations

The PSC Managers will summarise and make public, on an annual basis, the top five investment firms in terms of trading volumes where it transmitted or placed client orders for execution in the preceding year and information on the quality of execution obtained for each class of financial instrument.

The information will be made available on the Pollen Street Group website.

Upon reasonable request from a Client, the PSC Managers will provide its Clients or potential clients with information about entities where the orders are transmitted or placed for execution.

13. Client Disclosure and Consent

In the UK, the FCA’s Conduct of Business rules require that a firm must obtain the prior consent of its clients to the execution policy and that a firm must obtain the prior express consent of its clients before proceeding to execute their orders outside a regulated market or an MTF. The firm may obtain this consent either in the form of a general agreement or in respect of individual transactions.

The UK Managers will disclose the Best Execution Policy to and obtain express consent to execute orders outside a trading venue from its Clients.

Appendix I of the Best Execution Policy - Execution Venues (as at most recent policy update)

Infinity International

Natwest Markets

Silicon Valley Bank